An interesting aspect of financial calculations is becoming familiar with

the formulas involved, effectively learning to 'read' them. What is the source

of the difficulty, giving us such apparently complex formulas? The quite simple fact

that .95 * 105 does not give 100. It gives 99.75. Because the

reference number is now

larger than 100 ie 105. If I pay back ù 100$ at 5% after one year - 105$ - the percentage

of capital in the payment will be more than 95:

And the percentage of interest less than 5. For a loan being repaid monthly, this

situation will also hold.

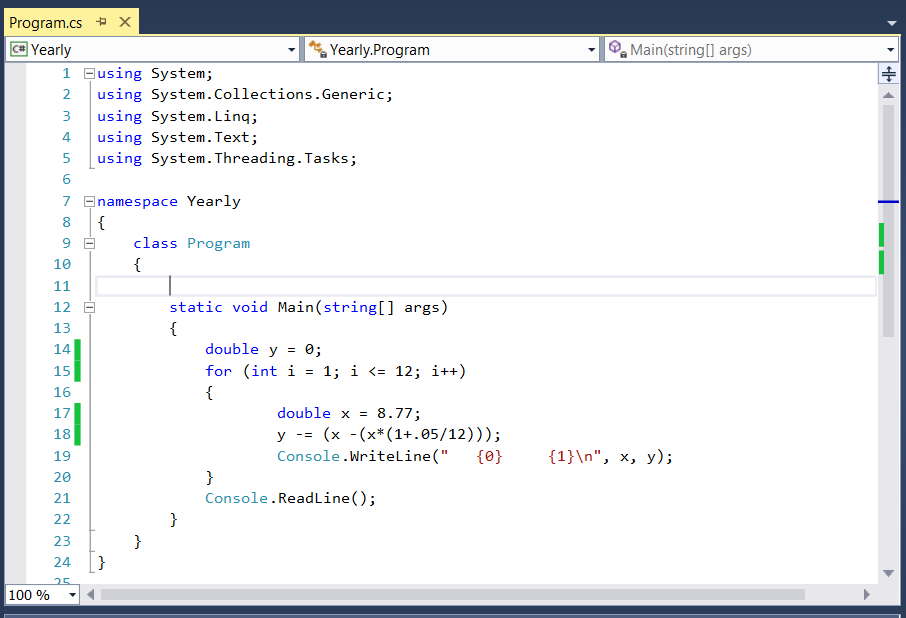

Working with the problem of a 1000$ loan at 5% repaid over one year, let's

examine the meaning of the numbers.

0.004167 5% over 12 months, per month

1.004167 a factor; adding interest to capital

(1.004167)^12 = above factor, iterated 12 times ( one year)

1.0512

1/1.0512 = the reciprocal; represents the capital part of payment

0.9513

1 - 0.9513

0.04867 the interest part of amount due for 1 month

The formula multiples the loan amount by the monthly interest rate, giving 4.17.

This is divided by the interest factor on the payment amount. The payment should be

85.68$ per month. (This should also be the last payment!!)

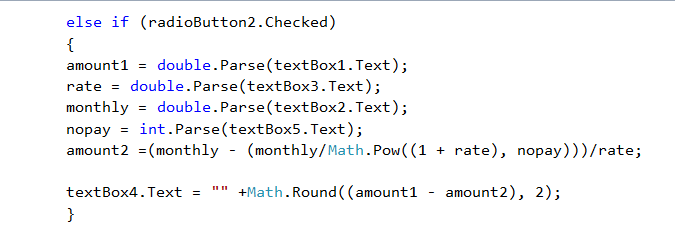

The first interest payment corresponds to a .0512 interest rate with respect to that

payment amount. The last - at 0.36 - to one of .0014617. One can check all those

in between using (1.004167)^11, (1.004167)^10 ... etc.

.png)

.png)

%2B-%2BCopy.PNG)

%2B-%2BCopy.PNG)

%2B-%2BCopy.PNG)

R.PNG)

.png)

.PNG)

.PNG)

.PNG)

.PNG)

%2B-%2BCopy.PNG)

.PNG)

.png)

.png)