Two incisive economic overviews from left-wing thinker, Yanis Varoufakis.

The comments and explanations are from Perplexity ai.

How did the European Central Bank manage to print 6 trillion euros?

Answer

The European Central Bank (ECB) did not literally "print" 6 trillion euros in the traditional sense. Instead, the ECB implemented various monetary policy measures to inject liquidity into the financial system and support the eurozone economy. These measures effectively increased the money supply, which is often colloquially referred to as "printing money." Here's how the ECB managed to create this large amount of liquidity:

Long-term Refinancing Operations (LTRO): In 2011, the ECB launched LTROs, providing low-interest loans to banks for up to three years. This program injected €489.2 billion into the banking system, with €325 billion going to banks in Greece, Ireland, Italy, and Spain.

Outright Monetary Transactions (OMT): Announced in 2012, this program allowed the ECB to purchase government bonds of eurozone countries, subject to certain conditions. While never implemented, it helped stabilize financial markets.

Quantitative Easing (QE): The ECB engaged in large-scale asset purchases, including government bonds and other securities. This expanded the ECB's balance sheet significantly.

Pandemic Emergency Purchase Programme (PEPP): In response to the COVID-19 crisis, the ECB launched a €750 billion emergency bond purchase scheme in 2020, which was later expanded.

Targeted Longer-Term Refinancing Operations (TLTRO): These operations provided banks with attractive borrowing conditions to stimulate lending to the real economy.

Through these various programs, the ECB effectively created a large amount of liquidity, supporting the eurozone financial system and economy during times of crisis. However, it's important to note that these measures were implemented over time and not as a single act of "printing" 6 trillion euros.

Is the argument presented in this video factually correct? (video 1)

Answer

Yanis Varoufakis's argument in the video is a critique of the European Central Bank's (ECB) monetary policies and their socio-economic consequences. While his claims are rooted in real economic events, the factual accuracy of his interpretation depends on the context and perspective.

ECB "Printing" €6 Trillion: The ECB did inject trillions of euros into the financial system through monetary policies like quantitative easing (QE) and long-term refinancing operations. This money was primarily used to stabilize financial markets by purchasing government and corporate bonds, providing liquidity to banks, and lowering borrowing costs. However, it was not literally "printed" in physical currency but created digitally.

Funds Benefiting Bankers: Varoufakis argues that these funds disproportionately benefited banks and large corporations rather than being directed toward productive investments in the real economy, such as infrastructure or technological innovation. This critique aligns with broader concerns about QE exacerbating wealth inequality by inflating asset prices (e.g., stocks and real estate), which primarily benefit wealthier individuals.

Economic Stagnation: His claim that this approach led to economic stagnation is a matter of debate. While QE helped prevent deeper recessions in the eurozone, critics argue that it failed to stimulate robust economic growth or address structural issues like low productivity, underinvestment in innovation, and rising inequality.

Stock Buybacks: The assertion that much of the liquidity was used for stock buybacks is partially true for corporations that benefited from low borrowing costs. However, this trend is more pronounced in the U.S. than in Europe, where strict regulations limit such practices.

Broader Implications: Varoufakis connects these policies to political fragmentation and Europe's declining global competitiveness, particularly in emerging technologies like AI and green energy. While these links are plausible, they involve complex socio-political dynamics beyond monetary policy alone.

In summary, while Varoufakis raises valid concerns about the distributional effects of ECB policies and their long-term impact on Europe's economy, some aspects of his argument—such as the exclusive blame on monetary policy for economic stagnation—may oversimplify a multifaceted issue.

Economics; is it an accepted view that a higher-valued currency leads to lower investment in a country's productive capacity? (video 2)

Answer

The relationship between a higher-valued currency and investment in a country's productive capacity is complex and not universally accepted as a direct cause-and-effect scenario. However, there are several economic arguments that suggest a strong currency can potentially lead to lower investment in domestic productive capacity:

Reduced export competitiveness: A higher-valued currency makes a country's exports more expensive for foreign buyers, potentially reducing demand for domestically produced goods and services. This can discourage investment in export-oriented industries.

Cheaper imports: A strong currency makes imports less expensive, which can lead to increased competition for domestic producers. This may reduce incentives for local companies to invest in expanding or upgrading their productive capacity.

Profit impact on multinational corporations: For companies with significant overseas operations, a strong domestic currency can reduce the value of foreign earnings when converted back to the home currency. This might lead to lower overall profits and potentially less capital available for reinvestment.

Attractiveness of foreign investments: A strong currency may make foreign assets appear relatively cheaper, potentially encouraging domestic investors to allocate capital abroad rather than investing in local productive capacity.

However, it's important to note that currency strength is just one factor among many that influence investment decisions. Other considerations include:

Interest rates and monetary policy

Overall economic growth and stability

Regulatory environment and ease of doing business

Technological advancements and innovation

Labor market conditions and productivity

Additionally, a strong currency can have some positive effects on investment:

Lower costs for imported capital goods and raw materials, which can benefit certain industries

Increased purchasing power for domestic consumers, potentially stimulating demand in some sectors

Attraction of foreign capital due to perceived economic strength and stability.

In conclusion, while a higher-valued currency can create challenges for domestic investment in productive capacity, it is not universally accepted that it always leads to lower investment. The overall impact depends on the specific economic context, industry dynamics, and policy responses to currency fluctuations.

Are there documented recent examples of American companies buying their own stocks to make the value go up?

Answer

Yes, there are documented recent examples of American companies buying back their own stocks, which can potentially increase the stock's value. Here are some notable examples:

Oracle Corporation: On March 10, 2025, Oracle announced a $154.50 million stock buyback.

Costco Wholesale Corp.: As of February 28, 2025, Costco repurchased $206.05 million worth of its own shares.

Apple: In the third quarter of 2024, Apple spent $25.4 billion on stock buybacks, which was a 19.2% increase from the previous quarter.

Alphabet (Google): Also in Q3 2024, Alphabet spent $15.3 billion on buybacks, although this was a 3.2% decrease from the previous quarter.

Hewlett Packard Enterprise: On March 6, 2025, HPE reported a $52.16 million stock buyback.

These buybacks are part of a larger trend. For the 12 months ending September 2024, S&P 500 companies spent $918.4 billion on buybacks, up from $787.3 billion in the previous 12-month period.

Goldman Sachs estimates that companies could spend approximately $1.07 trillion on buying back their own stock in 2025.

It's important to note that while stock buybacks can potentially increase a company's stock price by reducing the number of outstanding shares and increasing earnings per share, they don't always lead to an immediate increase in stock value. The impact depends on various factors, including market conditions, investor sentiment, and the company's overall financial health.

Is this practice from the US considered disproportionate?

The practice of stock buybacks in the United States is indeed considered disproportionate by many critics and analysts. Here's why:

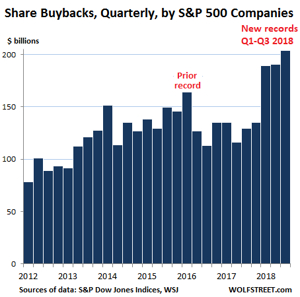

Scale: S&P 500 companies spent $4.3 trillion on buybacks between 2009 and 2018, equal to 52% of net income. In 2018 alone, buybacks reached 68% of net income1.

Comparison to dividends: The value of share repurchases by S&P 500 companies has exceeded total dividends every year since 19971.

Resource allocation: Critics argue that funds used for buybacks could be better invested in capital expenditures, employee training, or other initiatives that contribute to long-term competitiveness1.

Income inequality: Buybacks are seen as exacerbating wealth disparities, benefiting wealthier stockholders and executives while providing limited benefits to workers1.

Historical context: Stock buybacks were considered illegal until 1982 due to concerns about market manipulation2.

Executive compensation: With the majority of executive compensation coming from stock options and awards, buybacks can be used to manipulate stock prices for personal benefit3.

Economic impact: Some argue that the massive scale of buybacks undermines equitable and stable economic growth, and contributes to financial fragility3.

Given these factors, many consider the current practice of stock buybacks in the U.S. to be disproportionate, favoring short-term stock price increases over long-term investment and broader economic benefits.

View More

Is this practice found in countries other than the US?

Yes, the practice of stock buybacks is found in countries other than the United States, although it is generally less prevalent and on a smaller scale. Here are some key points about stock buybacks in other countries:

Global Trends: Share buybacks have become increasingly popular globally, with the total value tripling in the past decade6.

Europe:

Buybacks are becoming more generous in Europe, with the total paid rising 2.9% to $146 billion in 20231.

Some European countries saw record levels of buybacks in 2023, including Italy, Spain, Norway, and Belgium1.

France, Switzerland, and the Netherlands had the largest value of shares repurchased in Europe1.

United Kingdom:

The UK is the largest non-US market for share buybacks, accounting for $1 in every $17 of the global total in 20231.

UK buybacks totaled $64.2 billion in 2023, equal to 75% of dividends paid1.

Asia Pacific:

Buybacks are less prominent in this region compared to the US and Europe1.

There were increases in buyback activity in Hong Kong and South Korea in 20231.

Comparison to the US:

While buybacks are growing outside the US, the scale is still significantly smaller. For example, in 2023, major EU companies spent $110.6 billion on buybacks, compared to $773.1 billion by US companies2.

Completion rates for announced buybacks tend to be lower outside the US. Non-US companies completed an average of 59% of announced buybacks after one year, compared to 75% for US firms3.

Increasing Popularity:

In 2022, buybacks became more widespread globally, with some markets narrowing the gap with the US7.

38% of large US companies bought back at least 1% of their shares in 2023, compared to 28% of the broader global market4.

While stock buybacks are indeed practiced in other countries, the US remains the leader in terms of scale and frequency of this practice.

No comments:

Post a Comment